Past

Commentaries

01/16/2025

Current Commentary

Dear Friends,

Look around, we’re in an epoch, a period of epic changes: social, economic, technological, geopolitical. With such turbulent changes market history suggests increasing risks and volatility. Technological disruption and demographics are disinflationary. But unsustainable debt threatens asset prices with systemic instability. Possible outcomes are default, dollar debasement and inflation.

Valuations

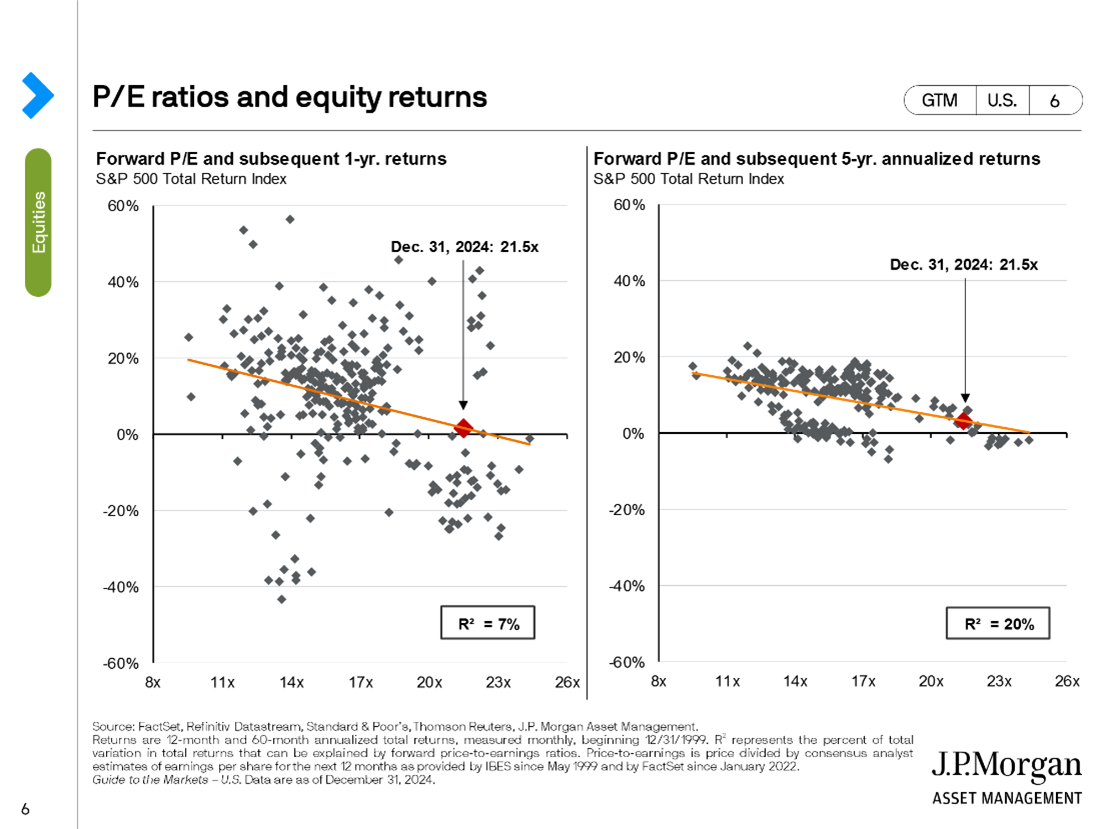

The S&P 500 trades at 30 times trailing 12 month (TTM) earnings with a dividend of 1.2%. Historical means are 16 and 1.2%. “Forward P/E ratios” (analysts’ predicted earnings) are also high, at 21.5. This doesn’t bode well for high future returns as the following chart indicates.

The reciprocal E/P, the earnings yield, is 3.2%. Compared with the 4.6% yield of the ten-year US Treasury, there is no equity risk premium, the higher return investors should receive for assuming stock market risk. There are some good reasons for sustained high P/E’s: broader participation in equity markets, fewer stocks in which to invest and the seduction of high variable returns compared to low fixed rate returns.

Earnings and quality of companies in the S&P 500 and NASDAQ Composite are wildly disparate. Almost half of NASDAQ stocks are still down more than 50% from their 2021 highs (Empirical Research). 40% of Russell 2000 small cap stocks are zombies, companies with debt service greater than cash flow.

The Magnificent 7 stocks are carrying the broader markets: NVDA, MSFT, AMZN, GOOGL, AAPL, META, TSLA. The leader of the 7 is NVDA. I started positioning NVDA in portfolios early in 2019. Earnings and revenues have not just grown, they’ve accelerated. NVDA is our single largest position despite recovering most of our original principal. Several months ago - before I took a deep dive researching artificial intelligence (AI) – I took a harder look at NVDA’s earnings, revenues, margins, book-to-bill and product development, seeking to answer the questions Is It Worth The Price and How Long Can This Last?

To get some historical perspective of the chip product life-cycle I referred to Intel (INTC) which used to dominate the market for chips. INTC has declined dramatically as NVDA has climbed relentlessly. NVDA dominates the global market for GPU’s (Graphic Processor Units). INTC used to dominate the market for CPU’s (Central Processing Units).

Over the last ten years INTC revs fell from $79B to $54B. P/E ranged from 49 to 9. Net income fell from $20B to $1.7B.

Over the last 4 years NVDA revs grew from $17B to $61B. When earnings are released the end of this month, trailing 12 months revenues will exceed $100B. P/E ranged between 86 and 14, currently 52. I looked at INTC and NVDA chip installations trying to estimate their life-cycle. The average, supported, functional life of INTC CPU’s is approximately 7 years. For NVDA GPU’s it is 8 years. This doesn’t address the ever-present likelihood of technological obsolescence.

NVDA has strong barriers to entry, including the systematic and capital commitments to their chips by its customers. NVDA chips for AI range from $30k to $70k; full server racks are estimated at $1.8M to $3M. This gives their installed base a certain amount of life extension – they’re too expensive to replace easily.

The problem NVDA has is a big one: they are sold out and cannot meet the demand. In any industry the result is the same: it puts competitors in business. MSFT, GOOGL and AMZN are scrambling to develop their own AI chips. Their biggest obstacle is that Taiwan Semiconductor (TSM) is currently the sole manufacturer for NVDA and the only manufacturer technically capable of producing AI chips. The company that builds the wafer fabrication equipment (WFE) for TSM is ASML, a Dutch company.

For the fiscal year ending next month I’m expecting NVDA earnings of $3 a share. At $133/shr that drops the P/E to 44. If EPS doubles to $6/shr in ’26 that drops the P/E to 22. Given the smashing success of their Blackwell chips and the lineup of powerful new products in development, it is simply too early in the installation cycle for the market to demand such a low valuation. At these earnings a P/E of 30 is still cheap, implying a price of $180 by 2026.

Artificial Intelligence

In November I attended Schwab’s annual Impact meeting, this year in San Francisco. It’s a four day convention of economists, accountants, asset managers, investment advisers, trust officers and all types of vendors, with lectures, seminars and presentations pertaining to current affairs and finance. I’ve only skipped it once in the 10 years we’ve used Schwab. I’m always afraid of what I might miss. This year I went with two objectives, to learn all I could about AI and Cybersecurity. It was worth the trip.

Most people are not aware of the extensive use of AI today. Its applications are expanding exponentially. A software engineering firm revealed that 70% of its code is produced by AI. It is being developed for the law profession for addressing routine legal problems. It is being tested for medical diagnostics and pharmacological applications. In fact, AI has become a general-purpose technology, like the steam engine, electricity and computers. It started with Open AI in 2015 and advanced with Alphabet’s Transformer architecture in 2017. It really took off with Open AI’s ChatGPT in 2022. Open AI was founded by Sam Altman and Elon Musk.

GPT is the acronym for Generative Program Training. Anyone can subscribe to ChatGPT and there are two levels of subscription. One is a closed set that only utilizes the data that you give it. The other is an open set that utilizes your data and any other relevant data on the internet to solve the problems you give it. You can talk to it. The program uses large language models to communicate effectively. This first phase of loading information is the training phase which requires heavy duty computing to gather massive amounts of data which can be translated and composed into grammatically correct reporting, i.e. plain English.

After training, the next phase is inference, where the model executes on the knowledge gathered in training. Training is like going to high school or college. Inference is like going to grad school or work. One is learning; the other is acting or producing. There are big opportunities in customized chips for inference, cheaper chips that require less power, designed for specific tasks.

It is AI that is driving the market for NVDA chips. We are probably 10 years away from full AI integration. Some tasks it will perform very well, others not so much. An error tolerance of 6% was suggested at one lecture. That is certainly not tolerable in manufacturing or medicine. When an AI model does not have sufficient data to solve a query it may give an utterly bizarre response. AI engineers call this “hallucinating.”

Although for most of us our lives are open books, I would never suggest giving your most personal information to an AI model. You are giving something and someone enormous potential control over your life and your identity. It could invite mischief. It’s dangerous.

Cybersecurity

The evolution of chips and code has enabled AI but also Cybercrime. Voices and human images can be reconstructed electronically. A sophisticated thief needs only a few sentences to completely reconstruct or synthesize your verbal language. The machine can atomize a vocal recording of as few as 30 syllables into millibytes of phonemes and then reconstruct them. The same technology applies to a video image. Not to suggest that these are the simple larcenies of “a thief.” This is an enormous, growing industry. The cost to synthesize a voice is $2 per second. To synthesize a video, $1,000 per second – but getting cheaper.

If you don’t recognize a voice on a phone call, answer with one word only, “YES.” If you suspect you are engaged with an AI conversation you can foil it with a unique personal question that only you would know, like, “Where was Aunt Gertie’s retirement party?”

According to Schwab, 10% of Americans are scammed annually. Scams have doubled from ’22 to ’23. There are 3.4 billion phishing scams emailed every day. Scams are easy because we volunteer too much information unwittingly. It is a dangerous, different world.

If you need to transfer funds or assets an email alone is not acceptable. You must call me and vocally give or verify email instructions. It is imperative that you notify me when you are out of the country. Your phone may not work abroad and I may not be able to verbally verify your email instructions. Use dual factor authentication wherever possible.

Outlook

2025 would be the third year of a bull market. That would be rare. It has only had three years in a row of double-digit gains twice since 1940. The first year of a presidential election cycle is not usually a strong year. The S&P 500 index is priced significantly higher than its historical mean.

CFRA research forecasts S&P earnings growing 13% in ’25, with InfoTech EPS up 20.1%; Industrial EPS up 16.8%; Communication Services EPS up 10.5%; Financials EPS up 7%; and Utilities EPS up 9.1%. CFRA sees the S&P at 6585 next December, up 11% from today’s 5937 close. I’ll take it. But…

The DEBT is not going away. Inflation is not going away. The Fed rate cut of .50% in September and .25% in December is clearly inflationary. It will not ameliorate the nation’s debt service, which is now larger than the defense budget.

I expect our system will provide in the long-term what it always has, greater purchasing power. There are great opportunities for making money.

Kind Regards,

Dennis M. O’Connor